Moedas estáveis, um tipo de token virtual apoiado por um ativo de reserva e geralmente atrelado 1:1 ao dólar americano, se tornaram um veículo fundamental para reduzir custos, acelerar as operações e melhorar a rastreabilidade em diferentes tipos de pagamentos transfronteiriços, incluindo remessas.

Avanços regulatórios, adoção em massa de plataformas que permitem essas transações com taxas baixas e adoção por usuários que desejam proteção em uma moeda mais forte, permitiram que as stablecoins se posicionassem como uma opção clara para a transferência de fundos.

Em economias emergentes, como as da América Latina e do Caribe, as stablecoins estão se tornando uma alternativa importante para as pessoas receberem remessas a custos mais baixos, especialmente beneficiando países afetados por depreciações, pressões inflacionárias ou mercados em que o sistema financeiro ainda cobra altas taxas por esse tipo de operação transfronteiriça.

Moedas estáveis estão vinculados a algum tipo de ativo real, o que significa que, ao contrário de outras criptomoedas, eles são menos afetado pela volatilidade e outros choques que impactam fortemente, por exemplo, o bitcoin.

De acordo com o Fórum Econômico Mundial (WEF), as stablecoins podem ser apoiadas não apenas por moedas fiduciárias, como o dólar americano ou o euro, mas também por mercadorias como ouro e outras criptomoedas.

Também existe a possibilidade de moedas estáveis podem estar vinculados a algoritmos complexos, projetado para equilibrar a oferta e a demanda.

Atualmente, as stablecoins mais populares são USDT (Tether), USDC (moeda em USD) e DAI, pois são amplamente utilizados para plataformas de pagamentos, remessas e finanças descentralizadas (DeFi).

Especificamente, o USDT se destaca por seu alto nível de liquidez, o que significa que sempre há um grande volume de compra e venda disponível. Isso facilita a troca rápida por outras criptomoedas ou moedas fiduciárias. Além disso, está presente em praticamente todas as bolsas de criptomoedas do mundo, o que a torna um dos principais canais para movimentar capital entre diferentes mercados e países.

Por sua vez, o USDC tem sido cada vez mais adotado por empresas e instituições financeiras, apoiado por auditorias regulares que demonstram que cada unidade é respaldada por reservas equivalentes, como dólares americanos e títulos do Tesouro dos EUA. Esse nível mais alto de transparência, combinado com o suporte regulatório nas principais jurisdições, deu à empresa a reputação de uma stablecoin segura e previsível.

Ambos contribuíram significativamente para a adoção de criptomoedas, fornecendo uma ferramenta confiável para realizar transações rápidas e de baixo custo.

Moedas estáveis têm o potencial de preencher a lacuna entre sistemas bancários tradicionais e o ecossistema criptográfico, à medida que as regulamentações nas principais economias, como os Estados Unidos, avançam para oferecer maiores garantias aos usuários.

Por esse motivo, empresas financeiras e não financeiras em todo o mundo estão buscando adotar stablecoins para otimizar as operações transfronteiriças, reduzir custos e melhorar a rastreabilidade de pagamentos internacionais.

Para moedas estáveis para ser realmente útil na prática, é essencial ter rampas seguras de entrada e saída, que são as pontes que conectam o sistema financeiro tradicional ao ecossistema digital.

Esses mecanismos possibilitam a conversão de dinheiro tradicional (como dólares americanos, pesos mexicanos ou pesos argentinos) em stablecoins por meio de transferências bancárias, cartões ou dinheiro.

Ao mesmo tempo, eles permitem que essas stablecoins sejam convertidas novamente em residente moeda para saques ou uso diário. Sem essas rampas, a adoção se torna mais difícil e a eficiência operacional é perdida.

Interruptor de entrada, que permite que empresas na América Latina transformem suas soluções de pagamento transfronteiriço, enfrenta esse desafio oferecendo uma infraestrutura integrada que permite às empresas gerenciar esse ciclo de forma rápida, segura e rastreável.

À medida que o mercado de stablecoin se expande junto com o crescente ecossistema de remessas, O Inswitch oferece uma plataforma financeira abrangente que permite que as empresas integrem serviços financeiros facilmente por meio de uma única conexão de API.

Com uma arquitetura modular baseada em nuvem, a plataforma garante uma implementação ágil, altos padrões de segurança e conformidade regulatória, além de abrir novas oportunidades de receita.

Também permite transações em várias moedas, fornece monitoramento em tempo real, oferece taxas de remessa competitivas e possui licenças MSB que abrangem todos os estados dos EUA.

Um contexto regulatório favorável

Recentemente, o governo dos EUA aprovou o chamado Lei Genius, que exige que os emissores mantenham o apoio em ativos líquidos e cumpram as licenças, ao mesmo tempo em que estabelece regras para proporcionar maior transparência no mercado.

“O Lei Genius prioriza a proteção do consumidor, fortalece o status do dólar americano como moeda de reserva e reforça nossa segurança nacional” de acordo com um boletim da Casa Branca. A nova estrutura também será “tornar os Estados Unidos líderes indiscutíveis em ativos digitais, trazendo investimentos e inovações massivos para o país”.

A aprovação deste regulamento é vista não apenas como um passo fundamental para o futuro das stablecoins, mas também como suporte para outros ativos criptográficos, associado à atual alta que levou o bitcoin a 117.000 dólares em 29 de julho.

O caminho para as stablecoins está apenas começando, mas considera-se que elas têm o potencial de transformar o setor global de pagamentos à medida que são implementadas em várias plataformas.

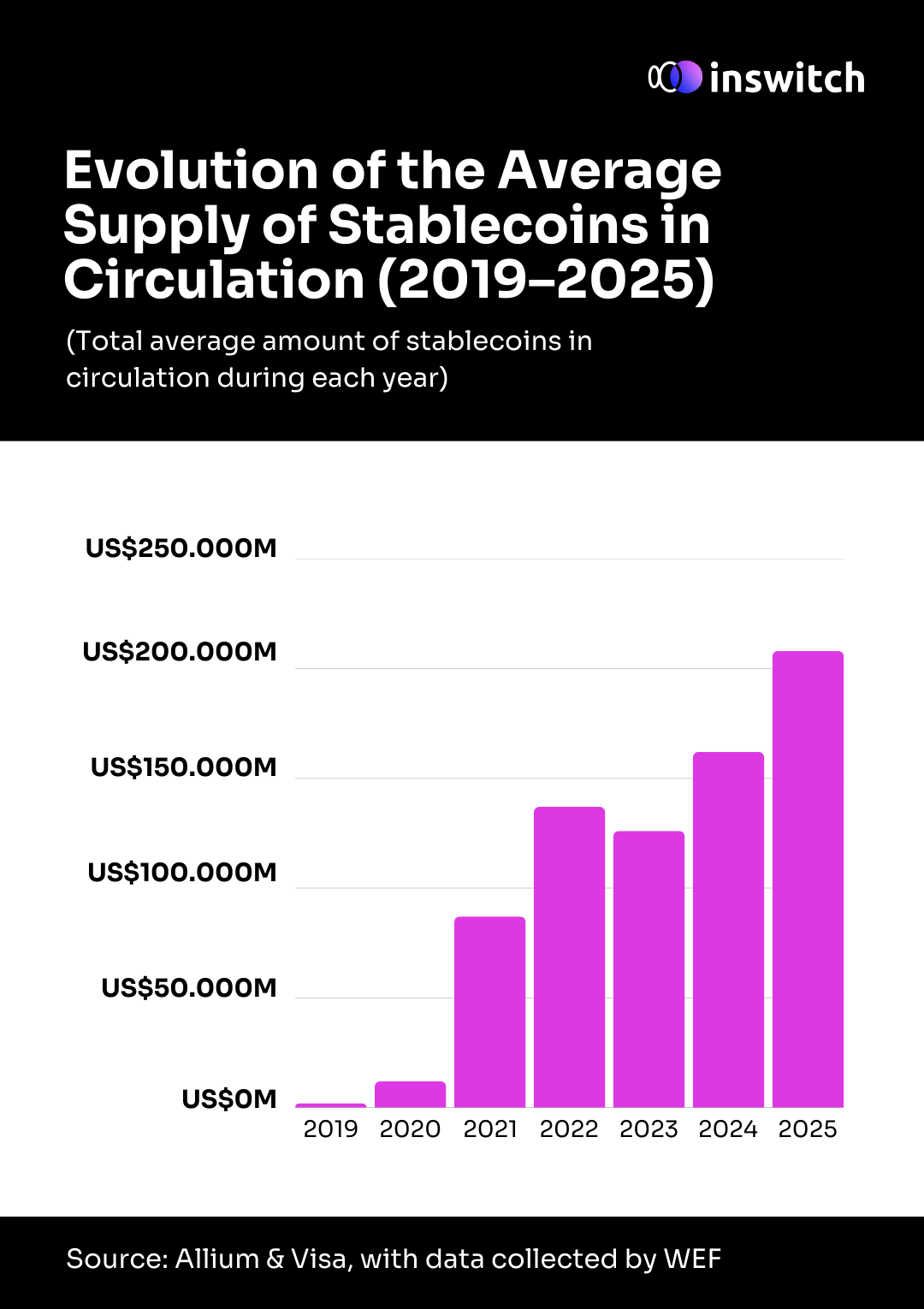

De acordo com dados compilados por McKinsey, “a circulação de stablecoins dobrou nos últimos 18 meses, mas elas ainda facilitam apenas cerca de 30 bilhões de dólares em transações diárias, menos de 1% dos fluxos monetários globais.”

No contexto comercial, o uso de stablecoins está se expandindo rapidamente no ambiente B2B porque eles oferecem uma solução eficiente e de baixo custo para pagamentos, especialmente em contextos internacionais.

Sua infraestrutura digital também facilita a integração em plataformas de tecnologia por meio de APIs ou contratos inteligentes.

Para empresas que operam em vários países, especialmente em mercados emergentes com sistemas bancários lentos ou caros, as stablecoins representam uma alternativa ágil para gerenciar pagamentos.

De acordo com um relatório da McKinsey, stablecoins podem representar uma opção mais eficiente em comparação com os mecanismos tradicionais de transferência de dinheiro, desde que a regulamentação o permita.

“Isso é especialmente importante nos corredores de remessas para trabalhadores migrantes e para resolver o problemas de pagamento enfrentados por pequenas empresas,” explica a consultoria.

No ano passado, as remessas para a América Latina e o Caribe chegaram a 161 bilhões de dólares, um aumento de 5% em relação a 2023, impulsionadas principalmente por migrantes nos Estados Unidos e na Europa, de acordo com o Banco Interamericano de Desenvolvimento (IDB).

Com o novo imposto de 1% sobre as remessas enviadas dos Estados Unidos, aprovado como parte da lei fiscal, as stablecoins podem se tornar uma opção mais acessível para os migrantes mitigarem os custos de envio mais altos.

Para cada 1.000 dólares enviados dos EUA, 10 dólares irão diretamente para cobrir os impostos.

O novo imposto de remessa nos EUA entrará em vigor em janeiro de 2026, então espera-se que os migrantes busquem alternativas mais baratas, com o risco de também recorrer a canais informais.

Nesse cenário, as empresas de serviços financeiros têm a oportunidade de atender a essas necessidades integrando soluções de stablecoin para facilitar as operações transfronteiriças.

O relatório McKinsey observa que as stablecoins se destacam por sua capacidade de fornecer assentamentos quase instantâneos, em comparação com 1 a 5 dias úteis em sistemas tradicionais.

Isso é combinado com um custo significativamente menor, com transações possíveis por menos de 0,10 dólares, em comparação com transferências internacionais (15 a 50 dólares por transação), CADA (0,20 a 1,50 dólares) ou cartões de crédito (1,5 a 3,5 por cento do valor da transação).

Em operações internacionais, as stablecoins permitem pagamentos sem fronteiras com comissões mínimas ou nenhumas de câmbio, eliminando a dependência de bancos correspondentes. Seu design digital também permite programabilidade avançada através contratos inteligentes, reduzindo os atritos e a necessidade de intervenção manual.

Outro ponto importante destacado pelos analistas é o transparência total fornecido pela tecnologia blockchain, com rastreabilidade completa de cada etapa da transação. Eles também reduzem riscos de liquidação operando diretamente peer-to-peer, sem intermediários.

Ao mesmo tempo, as stablecoins fornecem disponibilidade contínua, operando 24 horas por dia, 7 dias por semana, ao contrário dos sistemas bancários limitados por horas ou dias úteis.

Estratégias de riscos, conformidade e mitigação

Ao longo de sua história, o ecossistema de stablecoin também enfrentou vários desafios, incluindo o fraco KYC (Know Your Customer) e AML Processos (de combate à lavagem de dinheiro) realizados por alguns emissores e bolsas.

Como qualquer instrumento financeiro, as stablecoins não estão imunes ao uso por agentes maliciosos que podem utilizá-las para cometer crimes como lavagem de dinheiro, explorando lacunas nas políticas ecossistêmicas.

Isso pode resultar em sanções, contas congeladas ou auditorias para empresas, o que, por sua vez, pode levar a perdas financeiras e outras consequências que prejudicam a reputação corporativa.

Em geral, a implementação de políticas fortes de AML e KYC cria um ambiente mais saudável dentro do ecossistema de stablecoin, tornando as operações mais transparentes e rastreáveis.

Isso não apenas fortalece a confiança do usuário no uso de stablecoins, mas também fornece o suporte necessário para que eles avancem e se consolidem entre os atores institucionais, ganhando legitimidade e espaço no sistema financeiro tradicional.

O TRAMA observa que, embora o mercado tenha enfrentado desafios de liquidez e estabilidade desde o início, o ecossistema amadureceu com o tempo e várias stablecoins permaneceram consistentes.

Para mitigar os riscos na implementação de stablecoins, as empresas devem adotar uma abordagem baseada em riscos, com avaliações, medidas de resposta e recursos para enfrentá-los.

Ao mesmo tempo, é essencial aplicar a devida diligência completa do cliente e trabalhar com fornecedores regulamentados que estão em conformidade com os padrões KYC/AML.

Por exemplo, Interruptor de entrada detém licenças MSB nos Estados Unidos e integra processos de verificação de clientes, o que garante a rastreabilidade e a conformidade legal em todas as transações.

Além disso, fortalecendo cibersegurança interna e investir no treinamento da equipe — com medidas como firewalls, autenticação forte e prevenção de fraudes — é fundamental para minimizar as vulnerabilidades e maximizar as vantagens das stablecoins.

Estudo de caso: carteira com etiqueta branca e stablecoins

Em um ambiente em que agilidade e eficiência são essenciais para fintechs que operam internacionalmente, mais empresas estão buscando alternativas ao sistema bancário tradicional para gerenciar pagamentos e transferências.

Considere o caso de uma fintech que precisa distribuir 200.000 dólares em USDC para seus usuários.

Em vez de usar canais bancários tradicionais, opta por implementar um carteira digital de etiqueta branca através do Interruptor de entrada plataforma, que suporta dinheiro eletrônico, moedas locais e stablecoins, como USDC.

Por meio desse serviço, a empresa acessa a rede Inswitch para adquirir USDC por meio de um canal regulamentado, sob um acordo contratual.

A operação é executada em apenas algumas horas e resolvida em tempo real por meio de um serviço OTC (Over-the-Counter) regulamentado, com fundos creditados diretamente na carteira corporativa da fintech.

O chamado Serviço OTC é um canal privado por meio do qual as empresas podem adquirir ou liquidar grandes volumes de stablecoins diretamente com um provedor ou balcão de liquidez.

Em pagamentos internacionais, as operações OTC com stablecoins permitem que as empresas acessem melhores tarifas, liquidez instantânea e maior privacidade, tudo sob uma estrutura regulamentada que garante rastreabilidade e conformidade.

Todo o processo é apoiado por cheques corporativos KYC/KYB, Conformidade com AML e negociação transparente de câmbio.

Graças a essa solução, a fintech é capaz de envie fundos de forma rápida, segura e rastreável, sem depender de licenças criptográficas locais ou enfrentar os altos custos e atrasos do sistema bancário tradicional.

Este exemplo ilustra como o Inswitch permite que as empresas integrem stablecoins em suas operações financeiras de forma eficiente, garantindo a conformidade e otimizando os fluxos de caixa.

Como o Inswitch habilita essa tecnologia com segurança

Interruptor de entrada oferece infraestrutura financeira avançada que permite que empresas latino-americanas, como fintechs, plataformas de remessas ou transmissores de dinheiro, usem moedas estáveis e execute cpagamentos transfronteiriços de forma eficiente, segura e sob regulamentação.

A plataforma é construída em um Arquitetura baseada em API, o que facilita a integração de serviços financeiros em carteiras digitais, aplicativos móveis, sites ou até canais como o WhatsApp.

Isso permite que as empresas mantenham suas identidade de marca com uma solução de carteira de etiqueta branca personalizável.

O interruptor mantém Licenças MSB que fornecem cobertura regulatória em todos os estados dos EUA, permitindo operações com total conformidade legal nos dois lados da transação.

Ele também integra Ferramentas de verificação KYC/KYB, monitoramento de fraudes em tempo real e controles de conformidade, garantindo segurança em todas as transações.

Na prática, isso significa que uma empresa pode financiar operações nos Estados Unidos usando cartões, transferências ACH, carteiras, cheques ou até mesmo dinheiro e, em seguida, enviar esses fundos como stablecoins (como USDC) por carteiras seguras e em várias moedas com transferências instantâneas.

Por meio de parcerias com redes globais, como Mastercard Transfronteiriço, a Inswitch estende seu alcance para mais de 30 países, com mais de 250.000 pontos de saque e alianças com mais de 160 bancos, expandindo as possibilidades de uso e conversão de fundos.

Em resumo, o Inswitch permite o uso de stablecoins como parte de uma solução moderna, regulamentada e modular que simplifica os pagamentos internacionais, protege todas as transações e permite que as empresas expandam os serviços financeiros em toda a América Latina e além.

.png)