Real-time payments (RTP) have opened a new dimension for the gig economy. Couriers, freelancers, and digital platform workers can now receive their income 24/7, improving liquidity and granting greater financial autonomy.

The expansion of instant payments reflects a rising demand for financial solutions that are flexible, secure, and suited to the dynamics of digital work amid the technological platform revolution.

As labor markets evolve and money transfer channels transform, gig workers increasingly need immediate access to their income, secure digital tools, and seamless ways to manage their money online.

In this context, digital platforms face the challenge of enabling instant income access through smart wallets that integrate currency conversion, instant withdrawals, and strong authentication.

Gig economy jobs include activities such as passenger transportation, product and food delivery, short-term accommodation rentals, and other tasks facilitated by digital platforms. They are characterized by being on-demand, short-term, and managed primarily through platforms that connect service providers with customers.

In these models, integrating real-time payments is essential to ensure a frictionless experience.

For example, a mobility app could implement real-time payments so that drivers receive earnings instantly while users pay with local methods, reducing friction and simplifying expansion into new markets.

Similarly, a delivery platform could automate payments in seconds for thousands of couriers, granting them immediate access to their income while reducing operational costs tied to frequent transfers.

With adaptable infrastructure across countries, this type of solution promotes financial inclusion and accelerates expansion into new markets.

According to Mastercard and the Prime Time for Real-Time 2024 report, real-time payments are already available in more than 70 countries, processing 266.2 billion transactions in 2023, a 42.2% year-over-year increase.

GlobalData projects that global transaction volume will reach 575.1 billion by 2028, driven by a compound annual growth rate (CAGR) of 16.7%. Today, real-time payments represent 19.1% of all electronic transactions worldwide, and by 2028, that share is expected to exceed 27%, meaning more than one in four transactions will be real-time.

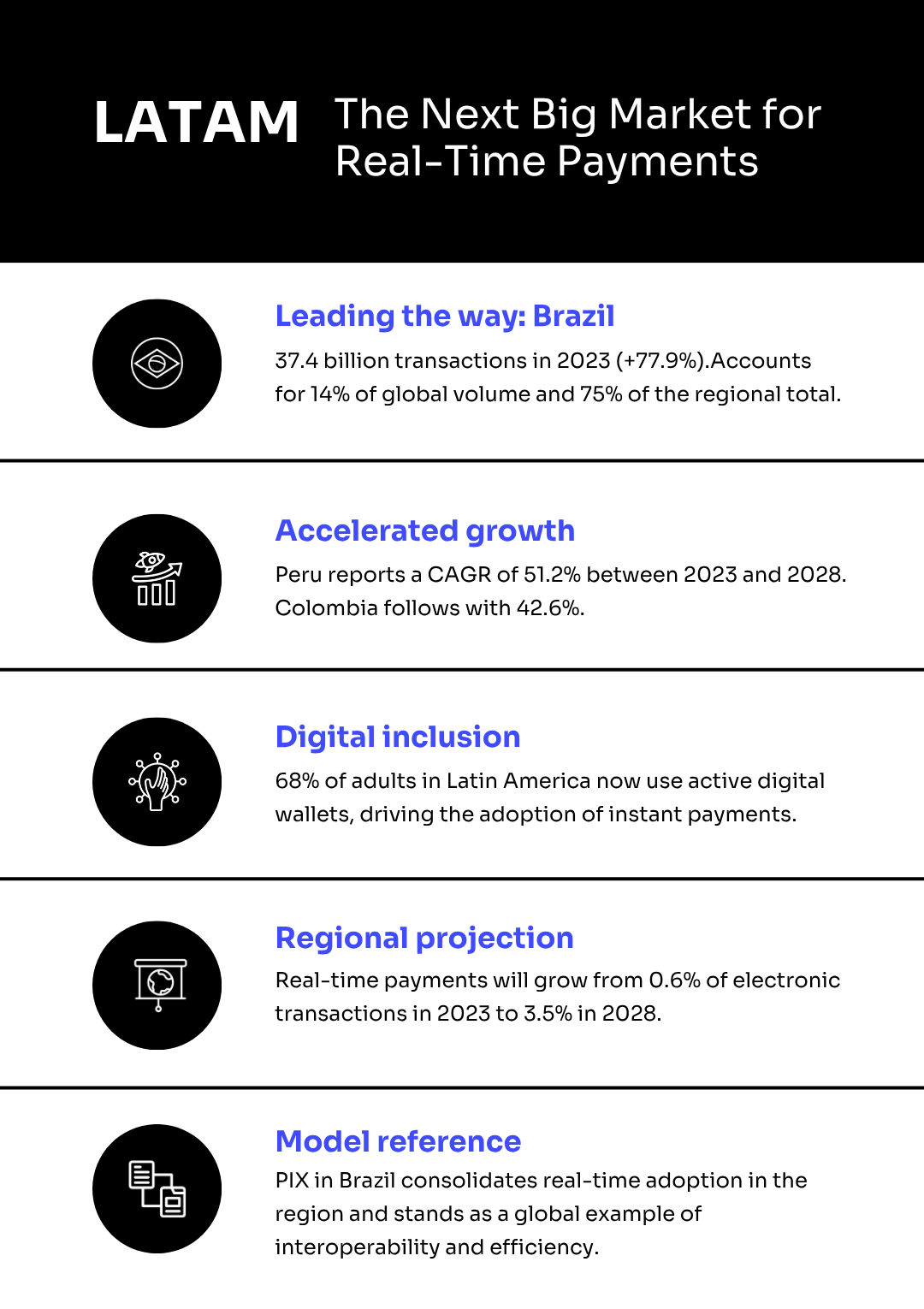

In Latin America, Brazil ranks as the second-largest market worldwide, with 37.4 billion instant payments in 2023, equivalent to 14% of global volume, thanks to the growth of the PIX system, which already accounts for 75% of all regional transactions.

Other markets such as Peru (51.2% CAGR) and Colombia (42.6% CAGR) lead regional growth projections for 2023–2028, while digital wallet adoption in the region has reached 68% of adults, highlighting the rapid maturity of the digital financial infrastructure.

The gig economy is opening new opportunities for digital payment expansion, as demand for these solutions grows across multiple economic sectors.

According to data cited by the World Economic Forum (WEF) and Business Research Insights, the sharing economy reached around USD 556.7 billion in 2024 and is projected to nearly triple by 2032, reaching USD 1.8 trillion.

Self-employed workers face unique financial challenges that require organized management of income, expenses, and tax obligations, issues that are increasingly being addressed by technology-driven solutions.

According to the World Bank, the gig economy represents up to 12% of the global labor market. Developed countries currently dominate the demand for temporary workers, but emerging economies are rapidly increasing their participation.

The World Bank also estimates that the global gig economy may include between 200 and 400 million workers. “In places where unemployment and informal labor are common, such as in Latin America, app-based delivery jobs offer new flexible employment opportunities,” it explains.

In 2023, the World Bank reported that 545 online labor platforms were operating globally, connecting workers and clients across 186 countries.

“Digital platforms can help increase visibility for informal workers, supporting efforts to expand social protection coverage for all,” said Namita Datta, lead author of the report at the World Bank.

To expand their potential, gig economy platforms must go beyond fast payments and inco rporate fraud monitoring and automated KYC/KYB verification, ensuring compliance and security.

Adopting local payment methods and enabling quick market expansion under a single technical integration can lower operating costs and improve user satisfaction and retention.

In this context, digital wallets have become a key tool for freelancers to participate in the global digital economy. They offer immediate access to funds and financial services at lower management costs than traditional banks.

According to Statista, digital payments through platforms like Apple Pay, PayPal, and Alipay are the fastest-growing payment method worldwide. Transactions made via digital wallets in e-commerce are expected to grow at a compound annual rate (CAGR) of 18% between 2024 and 2030.

In this landscape, Inswitch positions itself as a technological bridge. Its API-first platform allows gig economy and remittance companies to integrate instant payments, wallets, and cards quickly and without complex development.

Through this infrastructure, digital platforms can offer immediate, traceable, and secure payments, key elements in an environment where speed, trust, and user experience define loyalty and growth.

Inswitch’s proposal not only enables real-time payments but also connects workers, companies, and consumers in a more interconnected financial ecosystem, where liquidity and access to financial services are no longer barriers.

In this way, the company helps expand digital and economic inclusion, strengthening worker autonomy and driving new business opportunities in the era of superapps.

The rise of real-time payments not only transforms how gig economy workers receive their money but also opens the door to a new financial model based on integration.

Digital wallets are evolving beyond simple fund transfers to become superapps that offer savings, credit, insurance, and consumption within a single platform.

In this scenario, technology becomes the meeting point between users, businesses, and financial services and players like Inswitch play a decisive role by enabling connectivity across multiple solutions.

The convergence of payments, data, and financial services redefines inclusion, not just as access to a digital account but as full participation in the digital economy.

Latin America, in particular, stands out as fertile ground for financial innovation, where strategic partnerships—like those promoted by Inswitch—can make the difference between offering a service and building a network that empowers growth.

.png)